In partnership with

📢 A Message from our Sponsor

Why This Stock is Our Top Pick of the Month

Bank of America Predicts Gold Will Hit $3,000 by 2025 — This Gold Stock is Poised to Win.

As gold climbs once again, savvy investors are taking notice. This under-the-radar stock has already posted impressive gains and continues to attract strong insider buying, signaling significant growth ahead.

Don’t miss the chance to add this hidden gem to your watchlist before it breaks out again.

This is a sponsored advertisement on behalf of Four Nines Gold. Past performance does not guarantee future results. Investing involves risk. View the full disclaimer here: https://shorturl.at/73AF8

Welcome Back, Future Funder!

Let’s face it—early retirement might sound especially tempting after:

A grueling workweek,

A long, draining commute,

Or, worst of all, a call asking you to work this weekend.

But before you tell your coworkers to start planning your retirement party, there’s a lot to think about—starting with where you live.

Today, we’re taking a global journey to explore:

How early retirement (ER) and financial independence (FI) work in different countries,

Minimum retirement ages and how they differ worldwide,

The role of savings habits and average wages,

And their overall impact on achieving financial freedom.

Bon a petit! 🧑🍳

🥂 But first... happy hour highlights

Main Course: 🌴Early Retirement and Financial Independence

As it happens, retiring early might be a dream come true for many, but you’ll first need to make sure you’re sufficiently independent in the area of finances to make this happen with no headaches.

🌍 Retirement Ages Around the World

When it comes to official retirement age, where you live matters—a lot. In some places, you can begin drawing a pension as early as 55, while others require you to wait until your late 60s.

One key factor influencing these differences is global life expectancy, which has risen dramatically:

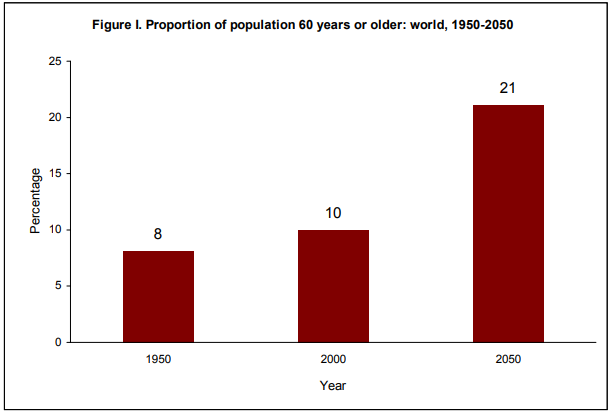

1950: Average life expectancy was 46.5 years

2000: This increased to 66 years

2024: We’re now up to 79 years

(Image credit: United Nations)

In response, many countries have revisited their retirement policies, adjusting minimum retirement ages to reflect longer lifespans.

Here’s a snapshot of current minimum legal retirement ages for a full pension:

France: 64 for everyone (starting 2030)

China:

55 for women in blue-collar jobs

58 for women in white-collar jobs

63 for men in any job

Iceland: 67

India: 65

Japan:

62 for women

64 for men

New Zealand: 65

Norway: 67

Saudi Arabia: 65

Turkey:

58 for women

60 for men

South Korea: 60

United States: 66

This variation highlights how cultural, economic, and demographic factors influence retirement policies worldwide.

As countries continue to adapt to changing demographics, keeping track of these shifts is essential for planning your early retirement goals!

🧾 The Realities of Achieving Financial Independence (FI) Globally

Early retirement often comes with a trade-off: less pension income. Achieving financial independence (FI) boils down to one simple formula:

Save more than you spend and invest the rest.

However, how easily you reach FI depends on three critical factors:

Wages

Savings rates

Living costs

Here’s a look at how this plays out in different countries:

1. United States: The Land of Hustle

Median Income: ~$80,610/year (household)

Savings Rate: ~4.6% (low compared to other countries)

FI Challenges:

High healthcare costs

Burdensome student loans

FI Strategies:

The FIRE movement encourages saving 50%+ of income.

Many rely on investments with a safe withdrawal rate of 4%.

2. Germany: The Land of Savers

Median Income: ~$54,000/year (individual)

Savings Rate: ~11% (much higher than the U.S.)

FI Perks:

Universal healthcare and strong pensions reduce reliance on personal savings.

A culturally ingrained focus on stability and future planning makes modest early retirement attainable.

3. Australia: The Balanced Approach

Median Income: ~$65,000/year (individual)

Savings Rate: ~20% (boosted by mandatory superannuation contributions)

FI Perks:

Employer contributions to retirement funds help Aussies save automatically.

A ‘bridge fund’ can cover early retirement expenses until retirees access their superannuation at age 60.

FI Challenges:

High housing and healthcare costs can slow down early retirement plans.

4. Japan: Playing the Long Game

Median Income: ~$23,000/year (individual)

Savings Rate: ~30% (the highest on this list)

FI Challenges:

A low culture of investing despite high savings rates.

High living costs, especially in urban areas.

FI Strategies:

Many opt for semi-retirement, balancing part-time work with leisure.

The ‘silver workforce’ often sees retirees returning to work to supplement income and stay active.

The path to financial independence looks different depending on cultural norms, economic conditions, and available resources.

🌟Key Takeaways:

Retirement Ages Vary

Legal retirement ages range from 55 in China to 67 in Norway.

Early retirees, however, often chart their own path by relying on personal savings and investments.

Savings Habits Matter

Countries like Japan (with a 20% savings rate) show how disciplined saving can make FI more achievable.

Still, cultural and economic factors, such as living costs, play a huge role in how far those savings go.

Investments Are Critical

The earlier your money works for you, the sooner you can leave the 9-to-5.

Popular investment strategies include index funds, real estate, and other reliable, income-generating assets.

Your Path May Vary

Factors like location, income, and lifestyle choices influence how quickly you can swap your desk for a deck chair.

Early retirement isn’t just about stepping away from the workforce—it’s about designing a life aligned with your dreams, values, and financial goals.

Wherever you are, remember: financial independence is a journey worth planning for.

Cheers to getting 1% better each week 🥂

P.S. - Are you working toward early retirement or already living the dream? Share your story - we’d love to hear your tips (and maybe take notes to share with our younger readers)!

📢 A Message from Brad’s Deals

From paper lists to Amazon Prime, times have changed.

While fast shipping and exclusive shows are well-known, these 10 hidden perks can take your membership to the next level.

🧙♀️ Your wish is our command

What did you think of today's email?

Thanks for reading.

Until next time!

Your friends @ Future Funders 🍽️

p.s. If you liked this newsletter, share it with your friends and colleagues here.