In partnership with

📢 A Message from our Sponsor

Get Reimbursed for Eligible Vet Bills!

Spot pet insurance plans can reimburse up to 90% of eligible vet costs.

Spot’s customizable plan options can help put money back in your pocket. Receive an additional 10% multi-pet discount for all pets enrolled after the first.

Independent and paid ad from Spot. Waiting periods, annual deductible, co-insurance, benefit limits and exclusions may apply. For all terms visit spotpetins.com/sample-policy. Products, schedules, discounts, and rates may vary and are subject to change. More information available at checkout.

Insurance plans are underwritten by either Independence American Insurance Company (NAIC 1126581. A Delaware insurance company located at 11333 N. Scottsdale Rd, Ste. 160, Scottsdale, AZ 85254) or United States Fire Insurance Company (NAIC #21113. Morristown, NJ), and are produced by Spot Pel Insurance Services, LLC. (NPN If 192463il5. 990 Biscayne Blvd Suite 603, Miami, FL 33132. CA License 116000188).

Welcome Back, Future Funder!

Owning a car isn’t just about getting from A to B—it’s a financial commitment that can significantly impact your wealth. Between depreciation, maintenance costs, and ever-changing gas prices, those shiny wheels might be quietly draining your wallet.

Here’s what we’re diving into today:

The real costs of car ownership in the U.S.

Depreciation dynamics: How it impacts your vehicle’s value—and how to minimize the hit.

Purchase options: Comparing new, used, leasing, and more to find the best fit for your finances.

Bon a petit! 🧑🍳

🥂 But first... happy hour highlights

On the surface, buying a car seems simple: pay a price and drive away. But when you dig deeper, the costs add up fast. Let’s break it all down:

📉 Depreciation: Your Car’s Value Over Time

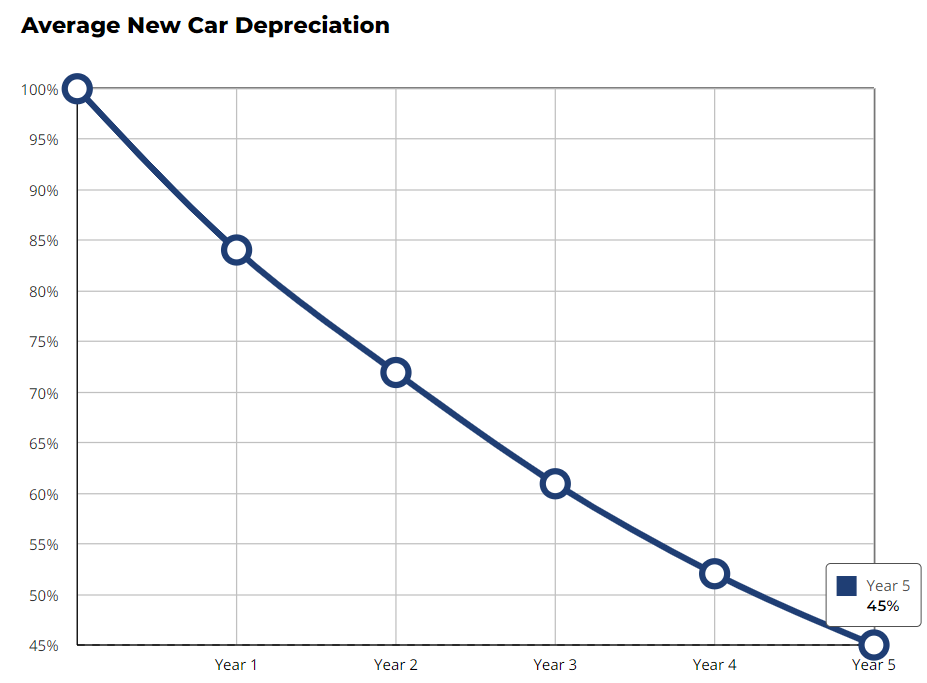

Depreciation is the single largest cost of car ownership, and it begins the moment you drive off the lot. Here’s how a typical depreciation curve unfolds for a new car:

The Depreciation Curve

Year 1:

Most cars lose 20–30% of their value within the first year.

Years 2–5:

Depreciation slows but stays steady, with cars losing about 15% annually.

By year 5, a car retains roughly 40–50% of its original value.

Year 6 and Beyond:

The curve flattens further, though steep declines can occur depending on mileage, condition, and market demand.

As of 2024, the average value loss per year—calculated for a car driven 75,000 miles over five years—is estimated at $4,680 annually (source: Kelley Blue Book).

(Image credit: Kelley Blue Book)

Pro Tip:

Consider purchasing a car after its 3-year lease return. These vehicles:

Have already absorbed the steepest depreciation.

Are still relatively new and often well-maintained, giving you the best balance of value and reliability.

Understanding depreciation can help you make smarter purchasing decisions and maximize your vehicle’s long-term value! 🚘

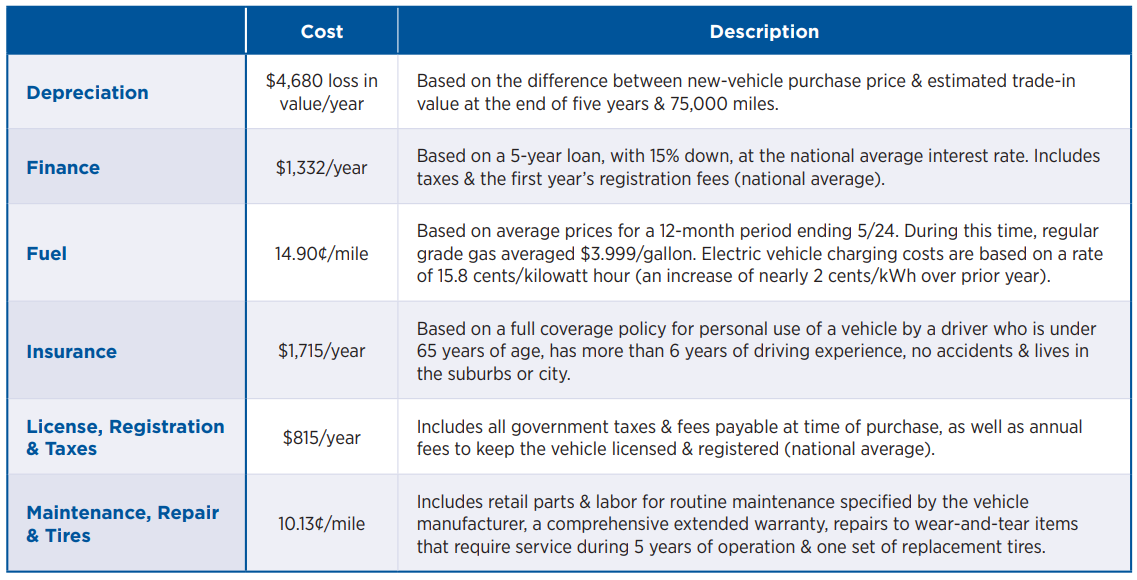

💸 The True Cost Breakdown

When purchasing a car, depreciation is only part of the story. Here’s a closer look at the additional costs that often fly under the radar:

1. Financing Costs

With average auto loan interest rates at 6.84% for new cars and 12.01% for used cars, financing can significantly increase your overall expense.

Borrowing to buy a car adds roughly $1,332 annually to the total cost.

2. Insurance

Annual premiums average $1,715, but this amount varies based on:

Location

Driver's age and experience

Vehicle type

3. Maintenance and Repairs

According to AAA, the average driver spends:

10.13¢/mile, which equals about $1,520 annually.

Costs increase as the car ages.

4. Fuel Costs

For U.S. drivers, fuel averages 14.90¢/mile, or nearly $4,000 annually for regular-grade gas.

Electric vehicle (EV) owners incur costs based on 15.8¢/kWh for charging.

5. Registration and Taxes

These fees average $815 annually, though electric and hybrid vehicles often face higher charges in some states.

Owning a car involves more than the sticker price—often overlooked, taxes, fees & registration hidden costs can add up to thousands annually.

Source: AAA

🚗 New, Used, Lease, or Alternatives?

Each car ownership option comes with distinct financial trade-offs. Here’s how they compare:

1. New Cars

Upsides:

Equipped with the latest features.

Comes with a full warranty for peace of mind.

High reliability.

Downsides:

Rapid depreciation (losing value as soon as you drive it off the lot).

Higher upfront costs compared to other options.

2. Used Cars

Upsides:

Lower purchase price than new cars.

Depreciation happens at a slower rate.

Downsides:

May require more repairs as the car ages.

Limited or no warranty, depending on the vehicle.

3. Leasing

Upsides:

Lower monthly payments compared to buying new.

Always driving a newer car without long-term ownership.

Downsides:

You’re paying for use, not ownership.

Comes with mileage restrictions and potential fees for exceeding them.

Upsides:

No maintenance or insurance costs.

Pay only when you need the car (calculated by time, distance, or demand).

Convenient for infrequent drivers.

Downsides:

Not practical for frequent drivers.

Costs can add up over time, potentially exceeding car ownership.

What Experts Recommend

For most buyers, a gently used car (about 3 years old) offers the best balance between cost savings and reliability.

🔗 Resources to Plan Ahead

Planning ahead for car ownership? These tools can help you make informed decisions:

1. Value Your Vehicle

Use resources like Kelley Blue Book (KBB) and Edmunds to estimate:

Trade-in value.

Private sale price.

Current market value.

2. Estimate Maintenance Costs

Check RepairPal and other repair cost databases to anticipate potential expenses for:

Regular maintenance.

Common repairs based on your car’s make and model.

3. Fuel Cost Calculators

Utilize AAA’s Gas Calculator to project annual fuel expenses.

Enter mileage and car type to get a realistic estimate tailored to your driving habits.

With these tools, you can better anticipate the true cost of car ownership and avoid all the joyous unexpected surprises 😉

🌟 Key Takeaways: Cars and Wealth

1. Depreciation Is King

Cars lose value rapidly, especially during the first few years.

Avoid buying new unless it aligns with your specific financial goals.

Insurance, maintenance, and fuel can quietly drain your wallet over time, often more than anticipated.

3. Buy Smart

A gently used car (about 3 years old, often after a lease) strikes the best balance between cost savings and reliability.

4. Consider Alternatives

Depending on your lifestyle, options like ridesharing or car subscription services could save money in the long run, especially for infrequent drivers.

Owning a car is often a necessity, but with smart choices, it doesn’t have to derail your wealth-building goals.

Cheers to getting 1% better each week! 🥂

P.S. – Have tips or tricks for cutting car-related expenses? Share your story, and we might include your advice in our next newsletter!

📢 A Message from CompareCredit

Top Card Offering 0% Interest until Nearly 2026

This credit card gives more cash back than any other card in the category & will match all the cash back you earned at the end of your first year.

🧙♀️ Your wish is our command

What did you think of today's email?

Thanks for reading.

Until next time!

Your friends @ Future Funders 🍽️

p.s. If you liked this newsletter, share it with your friends and colleagues here.